Impact of COVID19 on Bangladesh’s SME landscape

SMEs in Bangladesh contribute to 25% of the GDP and impact the livelihoods of 31.2 million people, making them crucial in job creation and economic growth. The global pandemic slowed down the economy as a whole, but SMEs were most brutally hit, and many are daily wage earners. In collaboration with Sheba, Light Castle Partner conducted a study with 230 respondents to analyze the COVID19 impact on Bangladesh’s SME landscape.

The study covered SMEs in multiple industries, mainly service and trade, agriculture, and retail. It focuses on the hurdles they faced due to the lockdown period and their businesses being shut. Some of the key findings were that SMEs lack access to finance, have limited linkages with supply and distribution markets, lack vocational and technical training for further growth, and barriers to enter the export market.

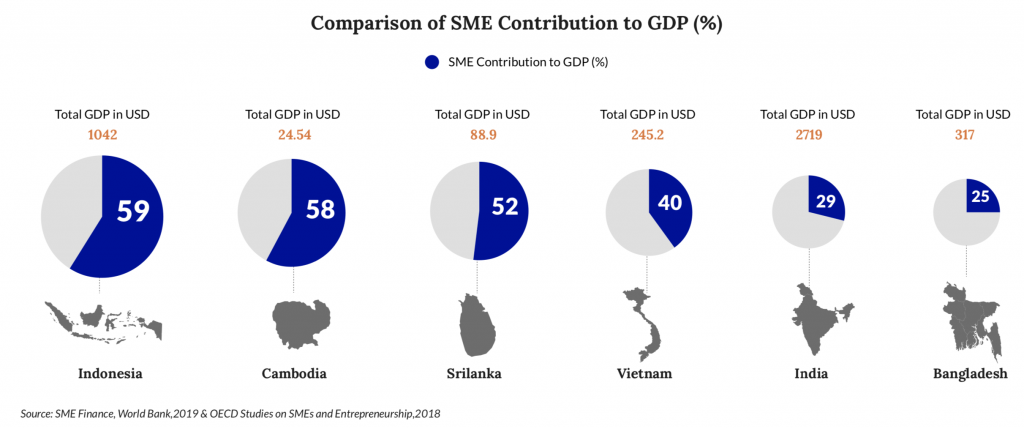

This cross-country comparison is shown to highlight the potential of SMEs in Bangladesh, as evident in our peer countries. Especially in Indonesia, SMEs have contributed significantly to their GDP with the support of a financing scheme by the government initiated in 2007. By 2018 $35 Billion was distributed all across the country with the help of venture capitals and non-bank financial institutions. This decentralization approach in financing SMEs also ensured high-quality credit with NPL rates as low as 0.24%.

Furthermore, the findings indicate that 52% of SMEs had completely halted their businesses. The majority were implementing strategies to bring marketing costs and operational costs to 0, and about half of them had layoffs planned. More than 70% of respondents were seeking working capital loans. Most SMEs sought soft loans, flexible installment packages, and government grants to survive downturns as such.

One case study shared in the report:

“A female entrepreneur from Rangpur manufacturing export oriented JDP has her orders at halt, thus, putting her in an acute liquidity crisis. Having salaries due for over 50 employees including both full time and part time, in addition to not having raw materials at hand for further production, a soft loan will help her to pay off her salaries and buy new raw materials.”

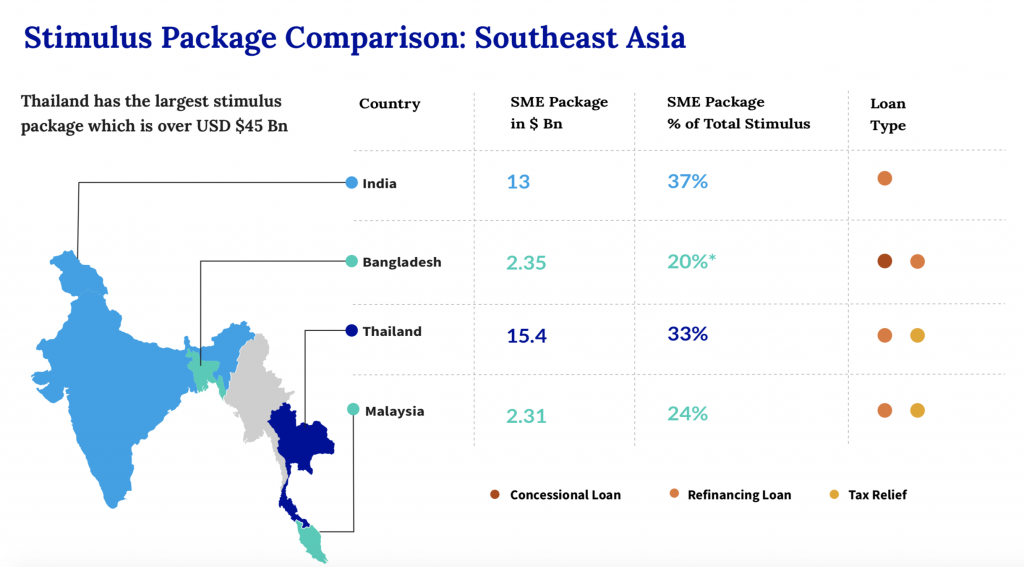

The report provides a breakdown of the Bangladesh Government’s stimulus package allocated for economic recovery. One of the issues highlighted is that only 9% of the fund is for CMSMEs, and they are repayable loans. Commercial banks are made responsible for credit profiling and absorbing all risks. This has proven to be a barrier to efficiently disburse the total package. Commercial banks are not equipped to reach rural unbanked populations where millions of SMEs operate. Our neighboring country India has allocated 13% of their total COVID stimulus package to SMEs and fixed their focus to take this opportunity to bring micro-entrepreneurs to the formal sector. Some key strategies have been making registrations convenient, nationwide access to the funds, and tax reductions.

According to the World Bank, there is a $2.8 Billion gap in SME financing in Bangladesh which is holding back their growth. The need for liquidity is now more than ever as we combat a global crisis. As suggested by LCP’s report, transparency in disbursement and collaborating with MFIs to extend the reach and providing cheaper working capital is the ultimate way forward to bring micro-entrepreneurs back to business. A handful of startups and initiatives apart from MFIs are also working to empower SMEs and can be leveraged to take the message to both formal and informal sectors. With the help of government policies, SMEs will be contributing significantly to the GDP and play a significant role in reducing poverty.

Read the full report here:

https://www.lightcastlebd.com/wp-content/uploads/2020/05/SME_WhitePaper.pdf

Secondary sources:

https://www.worldbank.org/en/topic/smefinance

ps://www.oecd-ilibrary.org/sites/67ce6854-en/index.html?itemId=/content/component/67ce6854-en